This month:

This month’s experts examine the potential of Vietnamese equities and UK financials, along with looking at key datapoints coming out of the US.

Expert investment views:

A case is made for bargains to be had in the UK banking sector before earnings accelerate

Vietnam’s virtues as a worthy addition to risk portfolios are set out

Key workforce and purchasing manager datapoints from the US are analysed

Featuring this month’s experts:

1. Time to rethink UK financials?

Insights from:

The past decade has proven to be a difficult one for the UK banking sector. The introduction of new regulations, revised capital requirements, the spectre of ongoing litigation and broad structural reorganisation have each taken their toll on the ability of traditional banks to generate and deliver returns to shareholders. As a result, the sector has been broadly out of favour and performance has been poor.

However, having comfortably weathered one of the most significant tests of their ability to withstand economic shock imaginable in the pandemic, we think there are many reasons to be more optimistic about the future of the sector from an investment perspective.

Having comfortably weathered one of the most significant tests of their ability to withstand economic shock imaginable in the pandemic, we think there are many reasons to be more optimistic about the future of the sector from an investment perspective

The accumulation of excess capital in recent years has been significant and the oft-cited headwind of persistently lower interest rates is also finally showing signs of abating (indeed the Bank of England raised interest rates by 0.15% at their December meeting). As such we expect earnings growth for the sector to accelerate markedly in 2022.

We do not believe this observation is accounted for by current valuations however, with the sector still trading at a significant discount to the wider market (mid-single digit PE multiples) as well as to its own estimates of book value.

Our contention is therefore that current valuations reflect the difficulties of the past and not the potential for significantly higher capital distributions in the future.

Adam Jones

Investment Manager – Family Office at Hottinger Investment Management

2. Vietnamese opportunity

Insights from:

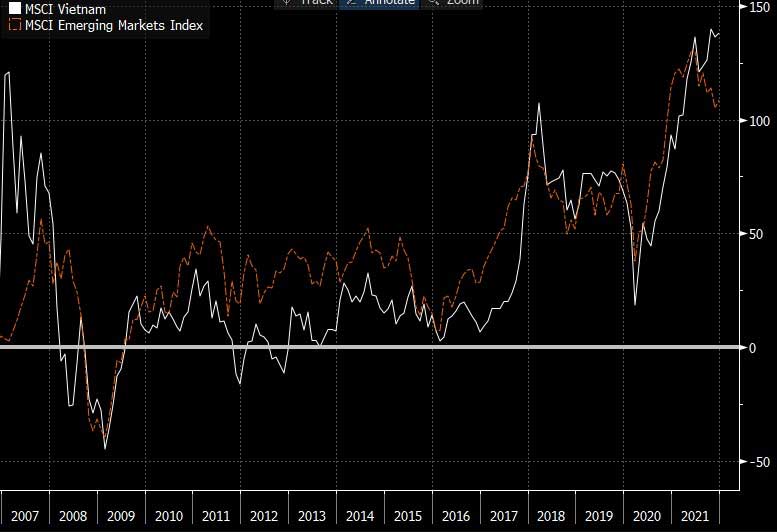

MSCI Vietnam vs MSCI Emerging Markets, 2007 to date in USD

Vietnam is benefitting from a young workforce and good geographic position (close to China), making it an attractive manufacturing location, particularly as the cost (political and otherwise) of manufacturing in China increases. Add to this a relatively benign Covid crisis, and a burgeoning consumer culture, and the reasons behind recent outperformance are clear.

Vietnam is benefitting from a young workforce and good geographic position (close to China), making it an attractive manufacturing location, particularly as the cost (political and otherwise) of manufacturing in China increases

Despite this, the larger UK listed investment trusts focussed on Vietnam still trade at significant discounts to their net asset values of around 15%. Perhaps it is the volatility of the market and its tendency to promise and disappoint. As an example, if you bought Vietnam in March 2018, after returns of +90% in the previous 15 months, you would have lost 40% to the lows of March 2020, and had to wait almost 3 years to have recouped your investment. Today, that investor would be up 122%, an annualised 14% return. Note that these are all index returns, whereas the larger trusts have significantly outperformed.

In conclusion, Vietnam is an exciting investment opportunity, yet one where repeated experience of boom and bust means that it pays to be patient. Today, valuations are reasonable at around 15 times earnings for a market growing at around 20% per annumii; a market worthy of consideration in a risk portfolio.

ii Source: Dragon Capital

Edward Allen

Private Clients Investment Director at Tyndall Investment Management

Top Tip

Lee Goggin

Co-Founder

3. Reading the runes on the US

Insights from:

It’s finally happening. The Fed is reaching for the punchbowl, not to refill cups but rather to start taking it away. Last week, they published the minutes from the December meeting: “Almost all participants agreed that it would likely be appropriate to initiate balance sheet run-off at some point after the first increase in the target range for the federal funds rate”. What does that mean in plain English? $8.3trn in Treasuries and Mortgages is just too big! So just like when your kids head off to university, it’s time to downsize. Bond yields rose and conversely the price for US Treasuries dropped. Tech shares also dropped while oil and financial stocks continued their run up.

For those of you who are fearing a jump in inflation, here’s the bad news: The US economy added a record 6.4 million jobs in 2021, rebounding strongly from unprecedented losses in the year prior due to the pandemic

And for those of you who are fearing a jump in inflation, here’s the bad news: The US economy added a record 6.4 million jobs in 2021, rebounding strongly from unprecedented losses in the year prior due to the pandemic. It is a good sign of economic recovery but will probably add to wage pressures. What’s the new rate? The unemployment rate fell to 3.9% in December while private payrolls rose by 807,000 – the strongest gain since May. How about the internals? A record 4.5 million Americans quit their jobs in November while openings remained elevated, highlighting persistent turnover in the labour market – I guess it’s a case of No Fear.

And finally, we all love a good PMI reading… US manufacturing printed 58.7 down from 61.1 in November. It’s down, but that’s still a great print (anything north of 50 is a positive read). How about services? Slightly cooler but still red hot. December declined to 62 from 69.1 a month earlier. What does all this mean? Omicron is negatively impacting the economy, but it remains strong all the same – c’mon guys, we will get through this.

Colin MacKenzie

Director, Investment Management at Arbuthnot Latham & Co., Limited

Important information

The investment strategy and financial planning explanations of this piece are for informational purposes only, may represent only one view, and are not intended in any way as financial or investment advice. Any comment on specific securities should not be interpreted as investment research or advice, solicitation or recommendations to buy or sell a particular security.

We always advise consultation with a professional before making any investment and financial planning decisions.

Always remember that investing involves risk and the value of investments may fall as well as rise. Past performance should not be seen as a guarantee of future returns.