Top Tip

Lee Goggin

Co-Founder

In a choppy environment, one market we are particularly keen on is the FTSE 100. Here are a few reasons why we think it remains well placed to outperform. That might sound strange in the face of a cost-of-living crisis and a lack of political leadership, but bear with us.

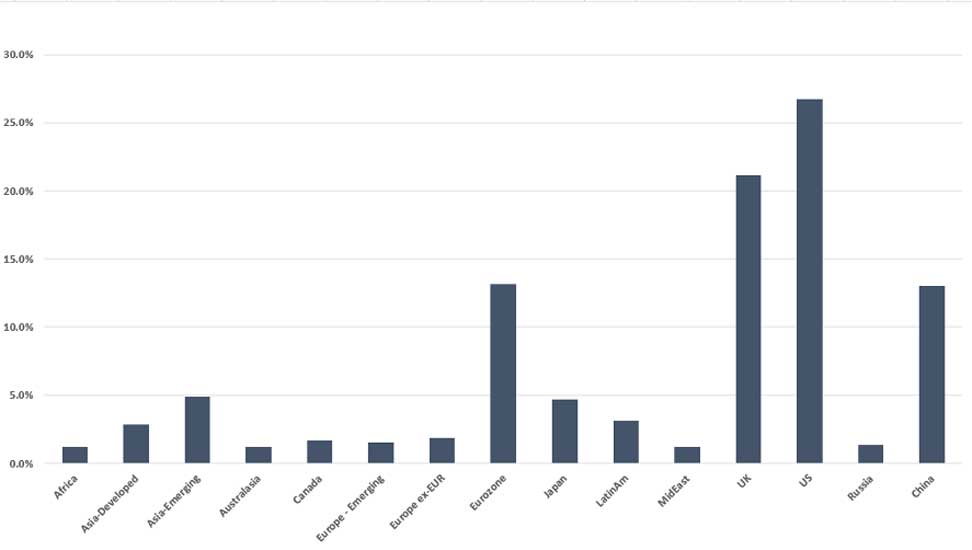

First, it’s crucial to realise that the FTSE has nothing to do with the UK economy (OK, maybe not nothing, but very little). The chart below shows the revenue exposure by region of the companies in the FTSE 100… the majority of sales come from outside of the UK. For many of the companies in the FTSE 100, UK economics is largely the “local news” at the end of the main bulletin.

FTSE 100 by Geographical Revenue Exposure

Source: Morningstar Direct

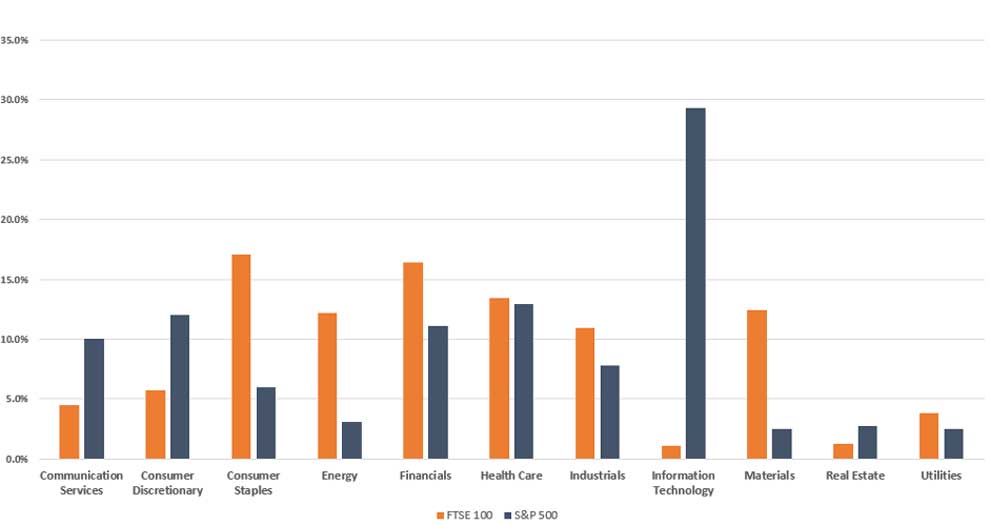

And the FTSE 100 has lots of exposure to sectors we like:

The first of which is energy. The FTSE is home to energy giants such as Shell and BP. With energy commodity prices where they are, these companies are extremely profitable and even after their outperformance, they are still relatively cheap.

Related are materials. The story for materials is similar to energy: they’re cheap, profitable companies. They also have the added kicker of being crucial to the clean energy transition. The infrastructure required to get the world meaningfully using renewables isn’t going to happen without vast amounts of copper, cobalt, and lithium.

The infrastructure required to get the world meaningfully using renewables isn’t going to happen without vast amounts of copper, cobalt, and lithium

Finally, healthcare, which we’ve been positive on for a long time. It has diversifying defensive properties. Not only that, but when combined with the developed world’s rising life expectancy and demand for healthcare, we think the sector is in a good place.

FTSE 100 vs S&P GICS Sector Exposure

Source: Bloomberg

Source: Bloomberg